The board question on the table

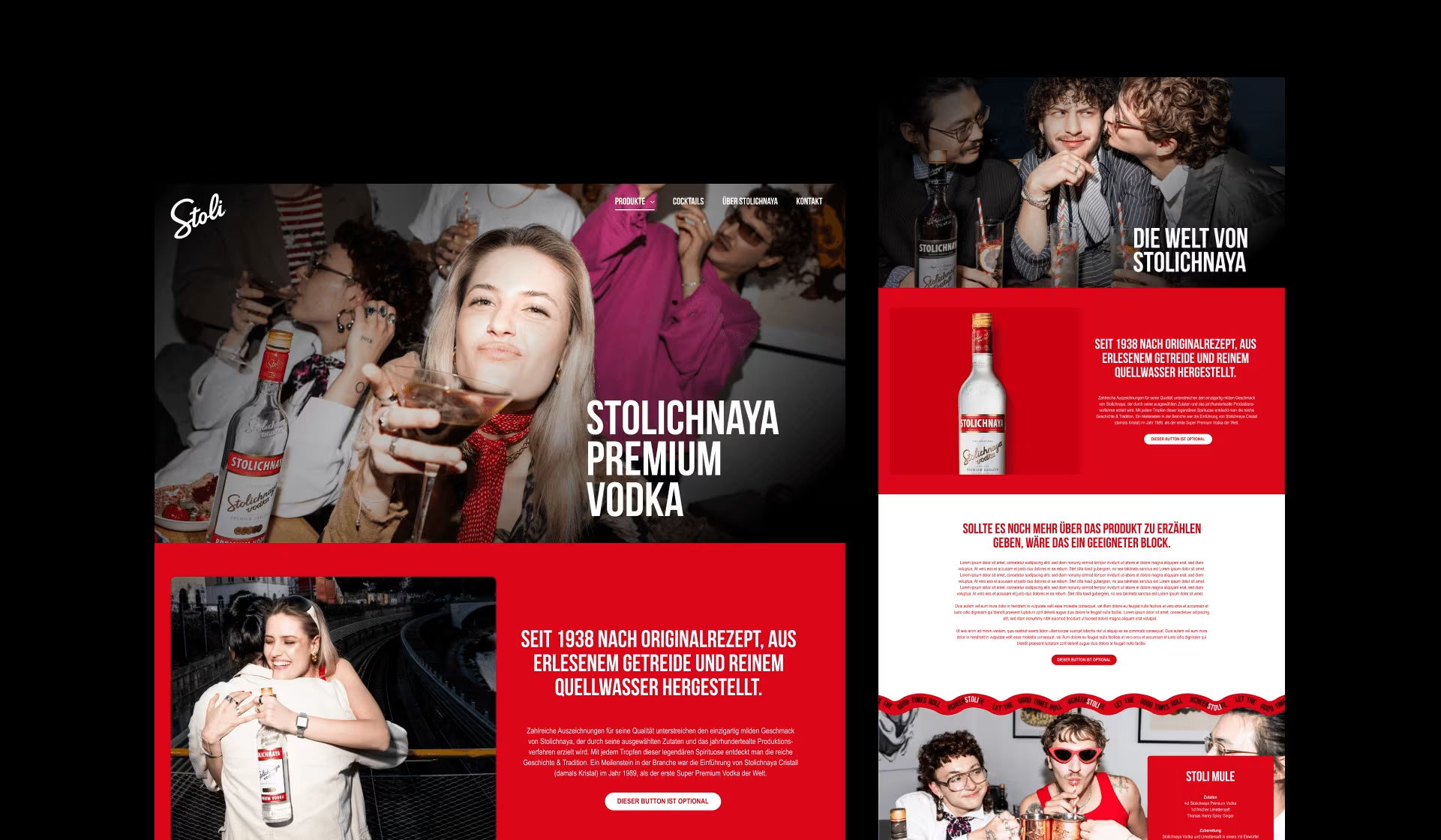

The founder of a premium spirits brand came in off the back of a record domestic year and wanted to put the US on the table for this cycle. Alfred took the ambition seriously and then made it concrete: the real cost of entry — three-tier distribution, state-by-state licensing, the depletion allowances and slotting fees nobody budgets for, and the eighteen months of cash burn before a single market turns. He laid out what the brand would be trading off to fund it, and what a stalled launch would do to the next raise. The question was never whether the US was the right market. It was whether this was the right year to spend the company's one shot at a first impression.

The reasoning

A market-entry decision is won or lost on timing, not appetite. The US would still be there in a year; the company's cash and its credibility with investors would not survive a launch that ran out of runway before depletions caught up. Alfred's case was simple: fund the launch from strength, not from hope. Enter with enough capital to hold shelf space through the slow quarters, or wait one cycle, bank the domestic momentum, and go in heavy when the balance sheet could absorb the burn. A half-funded launch doesn't buy you a smaller win — it spends your one shot at a first impression and leaves you raising into a stumble. In a market like this, discipline is the strategy, not the brake on it.